- Zuber Letter

- Posts

- Why Gen Z could be the next great generation

Why Gen Z could be the next great generation

If the younger generation plays its cards right, they could reach financial success faster than Millennials or Gen X.

Michael Zuber

October 25, 2024

Today’s newsletter is brought to you by Flock Homes!

If you purchased rental property before 2015, you'll likely pay thousands of dollars in taxes when you sell, not to mention lose your cash flow. An effective way to retire from the tenants, toilets, and trash of rentals has proved elusive—until now.

Join Flock Homes CEO Ari Rubin in an exclusive webinar recording to learn about the 721 Exchange tax and retirement strategy for landlords. Over 150 experienced landlords have successfully employed this strategy to minimize their tax burden, earn consistent cash flow without the stresses of ownership, and gain control over their liquidity and estate planning.

Flock’s team brings together decades of financial and real estate expertise from across institutions such as J.P. Morgan, State Street Global Advisors, and Progress Residential. Take advantage of this exclusive webinar now.

Why I think Gen Z could be a generation of winners

Did you know that at the age of 25, Gen Z owns more homes than Generation X and Millennials when they were the same age?

That fact is partially why I believe Gen Z, which includes people ages 12 to 27, has a chance to be the next great generation—if they play their cards right.

Last week, I spoke with Chad “Coach” Carson about how the younger generation can get ahead in the personal finance game.

Gen Z is the first generation that doesn’t think you have to go to college or you're a loser. That’s a game changer.

The stigma around not going to college for my generation and for millennials was pretty strong, I think after watching previous generations get crushed by student debt—without earning high enough salaries to make up for it—Gen Z is more open-minded about choosing other paths.

I think the younger generation will shock people and go into the trades (everything from video editing to welding and HVAC services) at unprecedented rates. These jobs are well paying, in demand, and don’t require you to take on a bunch of debt to get the needed skills. This big move to high-paying jobs and less debt will do a lot for the middle class.

On top of that, Gen Z gravitates towards “influencing.” This can support and supplement the development of their trade. If you master a skill, and share your experience with your trade online, by the time you're 35, you'll have a huge following and be considered an expert in the space.

Coach says there are a lot of trends that affect a household’s finances that Gen Z has different attitudes about, namely transportation. Gen Z is more likely to have one person in a household bike or walk to work than to have a car for each person going to work. Not having to pay for multiple car-related costs is a huge money-saver.

It’s also worth considering how prevalent self-driving car services might become, which could further eliminate the need for multiple cars per household.

Think about it:

Gen Z is avoiding college debt—that’s a win.

They are avoiding car debt—that’s a win.

They are gravitating towards six-figure trade jobs—that’s a win.

AND they are able to market themselves from a young age—that’s a win.

If you're in the Gen Z bucket and you're giving up, that's on you—the world is your oyster, so long as you do the work.

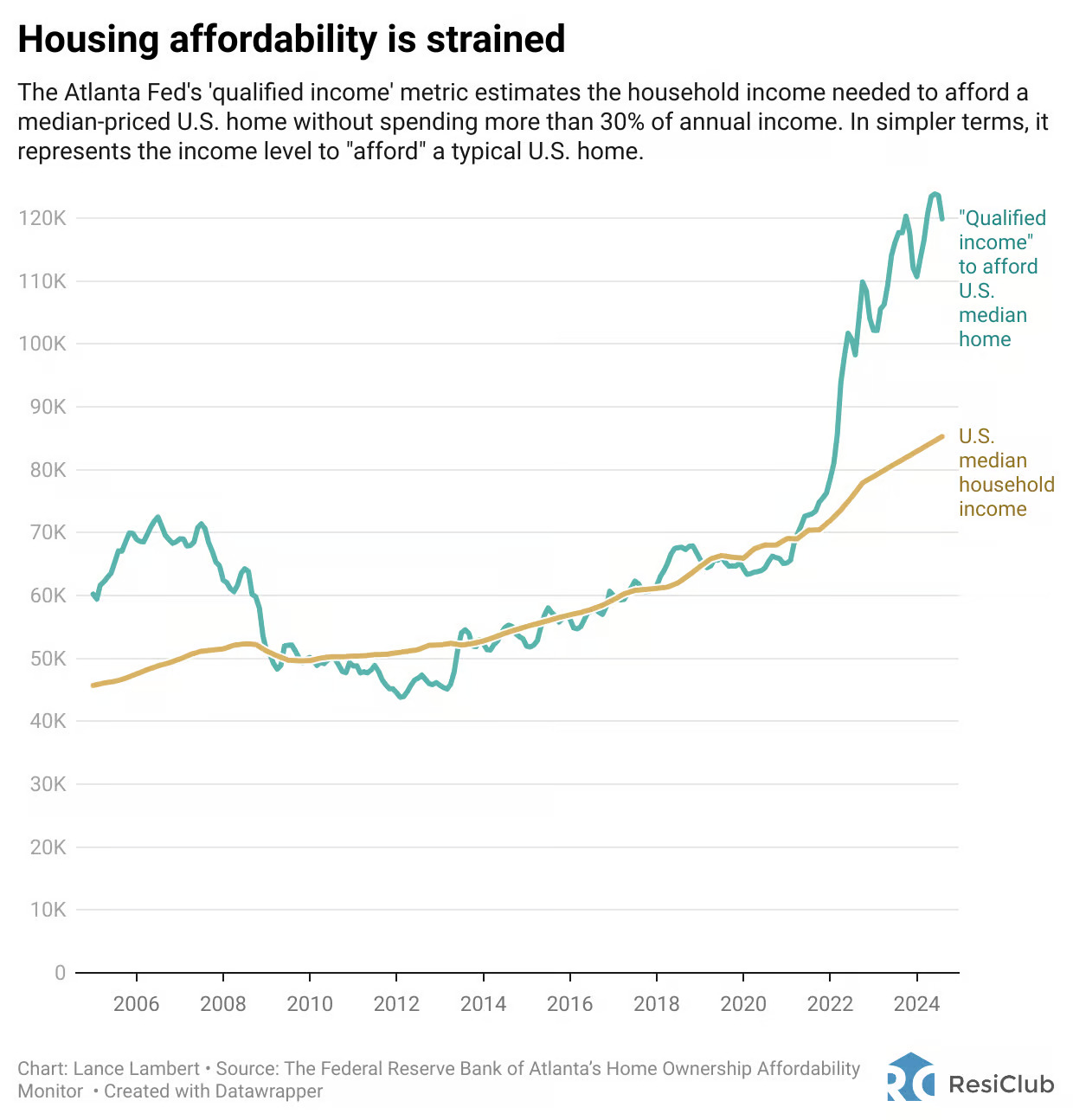

ResiClub chart of the week:

Last week, ResiClub’s Lance Lambert highlighted a recent analysis published by the Federal Reserve Bank of Atlanta that outlined just how quickly housing affordability has deteriorated these past few years.

Lance outlined a few key data points that say it all:

U.S. median household income in January 2020: $65,925

U.S. median household income in August 2024: $85,255.13

"Qualified income" to afford U.S. median home in January 2020: $64,257

"Qualified income" to afford U.S. median home in August 2024: $119,870

Number of the week: 3%

This week, Goldman Sachs published a report forecasting a sluggish stock market, with the S&P 500 annualizing 3% growth over the next decade. That’s a big drop from the annualized growth from the past decade, which is 13%.

For a while, I've been talking about home appreciation remaining pretty flat over the next three to five years, if not the rest of the decade.

When we think about the next decade, we have to remember we created a lot of asset inflation in the first couple of years of the 2020s which probably means that the rest of the decade is going to be flat-ish.

In the cases of stocks and real estate, you can't randomly pick stocks and expect everything to go up—we have to do the work, find value, and create our own opportunities.

Register for ResiDay

I want to remind my readers I’ll be speaking at the first-ever ResiDay, hosted by Lance Lambert’s ResiClub, in New York City on Friday, November 8th. That’s two weeks away.

There will be hundreds of influential housing single-family landlords, developers, lenders, and brokers who are shaping the future of residential real estate, homebuilding, mortgage lending, and build-to-rent. Several prominent real estate journalists will also be there.

The ResiDay discussion will center around where the U.S. housing market is now and where it will go from here.

Expect great conversation, networking opportunities, and just plain fun—I hope to see you there.