- Zuber Letter

- Posts

- What is the Fed most afraid of?

What is the Fed most afraid of?

Historically, kicking off a rate-cutting cycle with a 50 bps cut means trouble lies ahead—so what exactly is the Fed afraid of?

Michael Zuber

September 27, 2024

Before we get into today’s issue…

I want to remind my readers I’ll be speaking at the first-ever ResiDay, hosted by Lance Lambert’s ResiClub, in New York City on Friday, November 8th.

There will be hundreds of influential housing single-family landlords, developers, lenders, and brokers who are shaping the future of residential real estate, homebuilding, mortgage lending, and build-to-rent. Several prominent real estate journalists will also be there.

The ResiDay discussion will center around where the U.S. housing market is now and where it will go from here.

Expect great conversation, networking opportunities, and just plain fun—I hope to see you there.

Now let’s get into this week’s edition.

What is the Fed afraid of?

This month, the Federal Reserve cut rates by 50 basis points. I don’t think they would have done this unless they were afraid. But the big question is, what are they afraid of?

Are they afraid that the unemployment rate will rise from 4.2% to 4.4%, as is forecasted? Do they think that unemployment will take the elevator up and rise to 5% or 5.5% over the coming months?

In the past few months we’ve learned about commercial real estate taking significant haircuts, so are they afraid of the banking crisis 2.0? Has “extend and pretend” run its course and now the Fed is helping the banks recognize losses without going insolvent?

Is the Fed afraid of the election? Are they afraid of Trump winning? Are they afraid of Kamala Harris winning?

Is the Fed afraid of consumers simply retreating and halting their participation in the economy? Are they afraid of the U.S. dollar becoming too strong?

Frankly, there’s a laundry list of reasons the Fed could be afraid, and it certainly could be a combination of these things. But no matter the specific reason, I think it's really important to understand how out of the ordinary this Fed Meeting was.

Here are some key metrics:

Q2 2024 GDP (second estimate) is at 3%

4.2% unemployment

2.5% inflation rate for the 12 months ending in August 2024 (the lowest it’s been since 2021.)

The stock market keeps hitting all-time highs.

When you only look at these numbers, it is confusing that this is the economic backdrop where the Fed cuts 50 bps out the gate.

Jerome Powell talked up the economy quite a bit during the meeting, but I don’t buy that the Fed would do such a large rate cut if they weren’t afraid.

I think the Fed is looking out the windshield, not the rearview mirror. In other words, while the retrospective data points laid out above paint one picture, the Fed is more focused on what they see ahead—and they do not like what they see.

After all, until this week, there’s only been a handful of times in history where the Fed started its rate-cutting cycle with a 50 bps cut—usually when something is going wrong in the economy. The last time was at the onset of the Covid-19 pandemic in March 2020, and the time before was during the Great Recession in 2007.

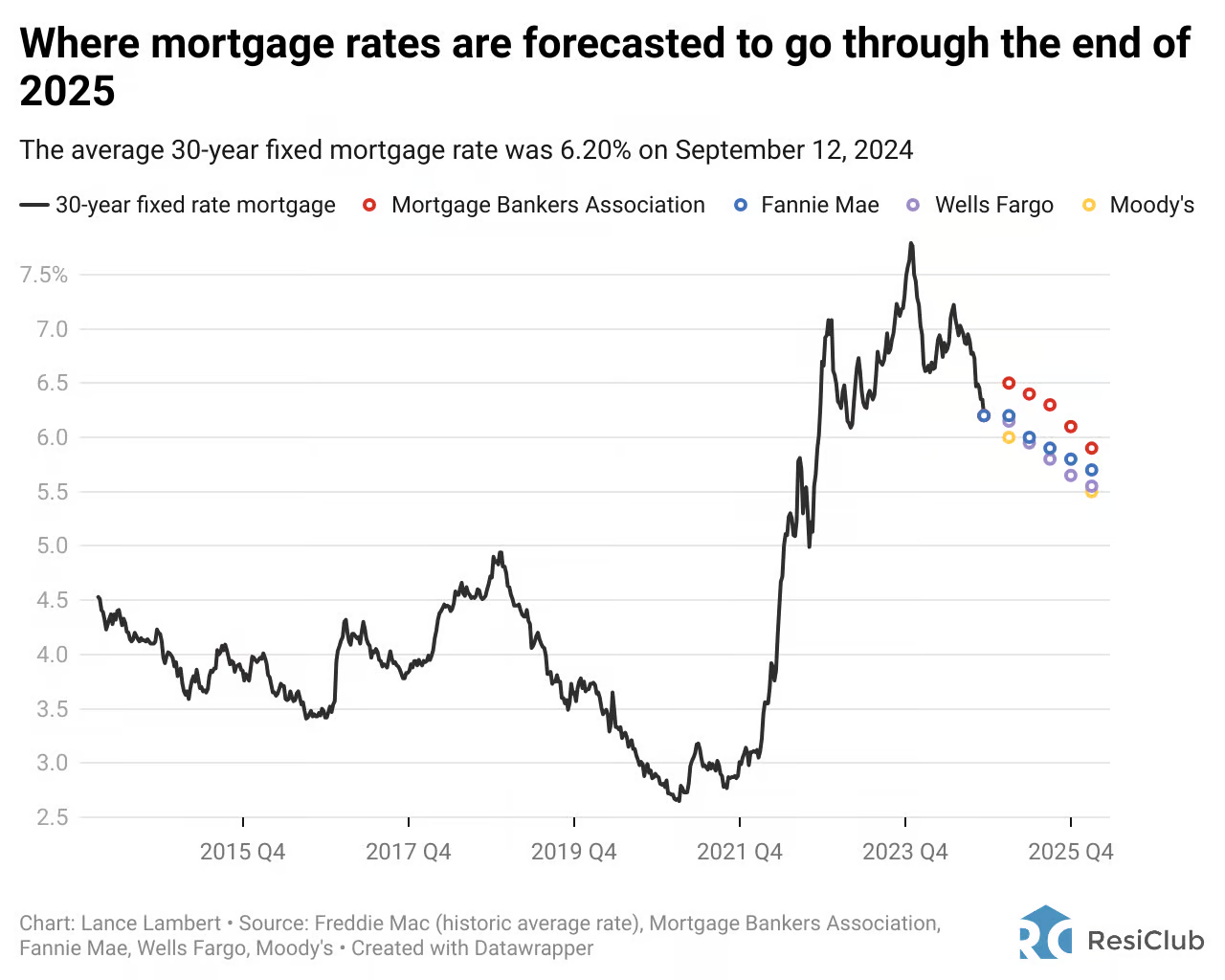

ResiClub chart of the week:

Recently, ResiClub’s Lance Lambert highlighted what the first round of rate cuts means for the U.S. housing market.

“While the Fed doesn’t directly set long-term rates and yields, including the 30-year fixed mortgage rate, its policy and the market’s assessment of future rates and the economy do have an impact,” Lance wrote.

Financial markets have already responded to labor market softening and anticipated Fed rate cuts as the average 30-year fixed mortgage rate decreased from a cycle high of 7.79% in October 2023 to 6.20% as of a couple of weeks ago.

With more rate cuts to come and less volatility in the market, groups like the Mortgage Bankers Association, Wells Fargo, Fannie Mae, and Moody’s all expect mortgage rates to come down even more, as Lance’s chart shows below.

Number of the week: 75

I recently read a gut-wrenching report that said the middle class can no longer plan on retiring at 65 and now should plan to work until 75. The essence of the story is that we are living longer, and our money is not lasting.

The fact is, especially as our population ages, we do not have enough tax dollars coming in to pay for Social Security and Medicare for everyone.

In the One Rental at a Time community, we know that despite this bad news, there’s a way to take matters into your own hands. Now more than ever, you should be securing your financial future and not relying on the current system to support you down the line.

The game is simple: live below our means and own and hold assets for at least a decade.

Join the One Rental at a Time Skool Community

The One Rental at a Time community on Skool is more than 270 members strong.

We’re creating more opportunities for you to interact with those who have achieved financial freedom through real estate investing.

Being surrounded by people at all stages of their real estate investing journey is crucial to your success, and joining us on Skool is an easy way to do just that.

It is only $20 to gain access to my monthly (or more) live streams as well as various millionaires answering your questions in real-time and connecting with people who can help you.

Learn more about how I am organizing the ORAAT Skool community content and calendar.